Helping more people save for retirement.

To get more people in the UK saving for retirement the Government has introduced new pension legislation bringing in automatic enrolment. Automatic enrolment requires all employers in the UK to offer their staff an opportunity to join a workplace pension scheme and automatically enrol any ‘eligible’ employees on to it. The employer and employee must then contribute a percentage of the employee’s salary in to the pension pot each pay period.

The government has set a legal minimum employer contribution percentage and a total contribution percentage that must be paid in to the pension pot. The employer has to contribute at least the minimum employer percentage and the employee must make up the shortfall between the total minimum and the employer percentage. You can find out more about how much you will need to contribute on the next page.

What happens next?

If you meet the eligibility criteria below, we will enrol you into our workplace pension scheme after a three months waiting period as permitted under the legislation. Our workplace pension scheme will be with Legal & General.

If you meet the following criteria, you are classed as an ‘eligible’ worker under automatic enrolment legislation and we are legally required to enrol you on to the workplace pension scheme:

• earn over £10,000* per annum

• ordinarily work in the UK and

• aged between 22 years old and state pension age

*this figure may change in the future.

If eligible, the next communication that you will receive will be your postponement notice, which will be sent via email. Please ensure we hold a valid email address for you so you do not miss receiving this communication.

If you wish to join the scheme during the waiting period, please follow the instructions under How to join.

What if I do not meet the criteria?

If you do not meet the criteria, you will not be automatically enrolled into the company pension, but you can ask to join the scheme if you wish to do so. If you earn above £6,240 per year (i.e. £120 per week/£520 per month), then we will also contribute to your pension pot. If you earn less than £6,240 a year, then just your contributions will go in to your pension if you ask to join.

How to join

If you do not meet the eligibility criteria and wish to join the scheme or you want to join during the waiting period, submit a written notice to us with your request. Please ensure that it includes the phrase, “I confirm I have personally submitted this application to join the Oxford Global Marketing workplace pension plan.”

What pension scheme will my contributions be paid to?

Legal & General (L&G) will be your pension provider. After you are enrolled, Legal & General will send you a welcome pack in the post.

Your welcome pack will be issued after the pension files have been processed, which will be the month following your enrolment. Please make sure we hold the correct address for you by checking the address on your payslip and let us know immediately if it needs to be updated.

Where can I obtain further details about the Legal & General Pension?

The following website will provide further information: www.legalandgeneral.com/wpp

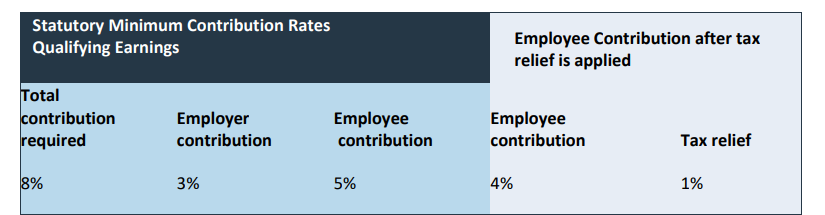

What contributions will you and Oxford Global Marketing make?

These percentages are the minimum amounts that have been set by the pension legislation. They do not apply to all of your earnings, but to your Qualifying Earnings. If you want to contribute at a higher %, let us know and we will adjust your contribution accordingly.

Qualifying earnings refer to a band of earnings between a set lower and upper value. In the current tax year, qualifying earnings are your annual earnings less the lower earnings threshold of £6,240 and up to a maximum limit of £50,270. The Department of Work & Pensions reviews qualifying earnings annually and the amounts may change in future. You can check the current band on TPR’s website by clicking here.

Qualifying earnings include Salary; Wages; Overtime; Bonuses; Commissions; Statutory maternity pay; Ordinary or additional statutory paternity pay; Statutory sick pay; And Statutory adoption pay.

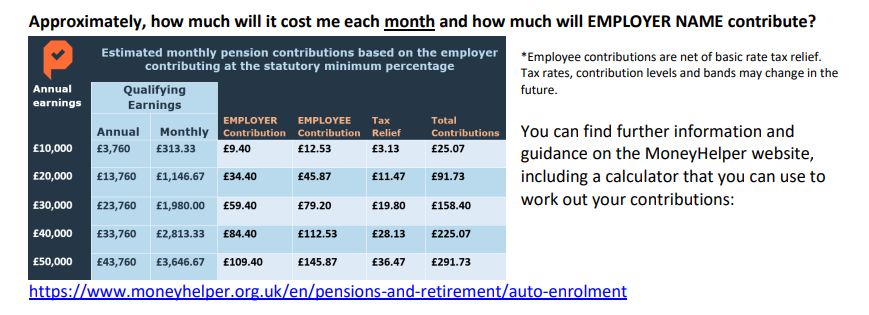

Example:

Ben is 25 years old and receives an annual salary of £20,000; his monthly earnings equate to £1,666.67. First, we work out his qualifying earnings by taking away the lower monthly level, £1,666.67 - £520 = £1,146.67 (Ben’s monthly pay does not exceed £4,189.17 so we do not need to take the upper level in to account).

• His employer will contribute £34.40 (i.e. 3% of £1,146.67)

• Ben will contribute £45.87 (i.e. 4% of £1,146.67)

• Tax Relief will equal £11.47 (i.e. 1% of £1,146.67).

In total, £91.73 will be paid in to Ben’s pension pot each month.

What happens if I don't want to be enrolled?

If you meet the criteria of an eligible worker, we are legally obliged to enrol you. You can however leave the pension scheme after you have been enrolled. Your paperwork from L&G will include instructions on how to do this.

Your letter from Legal & General will let you know how to opt out (i.e. leave the pension scheme) and the deadline for doing so (this will be around 30 days from when you receive your letter). If you opt out, your contributions will be refunded back to you through your next pay slip. Due to the time taken to process an opt out request, you may be deducted pension contributions for a second month, but as long as you opt out within the deadline, this will also be refunded back to you.

After the deadline has passed, you can ask to stop making further contributions to the pension scheme, but your contributions will not be refunded and will remain in your pension pot. This is known as ‘ceasing active

membership’.

You will be able to claim your pension when you turn 55 (the government proposes to increase this to age 57 from 2028).

Every three years, employers are required to re-enrol any eligible workers who opted out more than 12 months ago. This three-year cycle is based on the date they first began their Automatic Enrolment duties. Therefore, if you opt out, we may need to re-enrol you again in future. You would then receive a new welcome pack and have the option of opting out again.

You may ask to be excluded from automatic enrolment in the following exceptional circumstances:

1. You are a Director of a Limited Company or a Genuine Partner of a Limited Liability Partnership.

Or

2. You can provide evidence that you have built up pension savings above the Lifetime Allowance for HMRC

purposes and are protected from tax charges on those savings under HMRC’s primary, enhanced, fixed or individual protection requirements.

You will need to let us know if you wish not to be enrolled based on one of the above exceptions so that we may inform our payroll provider. If neither of these exceptions apply to you and you meet the eligibility criteria, you will be automatically enrolled. This is a legal requirement.

What do you need to do now?

We would like all employees to benefit from the contributions paid by Oxford Global Marketing Ltd and make the joining process as easy as possible. There is nothing for you to do at this stage. We have a ‘Q&A’ document that will provide further information. If you would like a copy or have any questions please contact Dan George on +44 7485 387172 or by email at d.george@oxfordglobal.co.uk